Review of the Week: September 11, 2023

As the dust settled from the Independence Day celebrations, the financial markets were ignited with key reports and developments. Inflation, both on the consumer and wholesale fronts, took the spotlight. Meanwhile, the housing market continued to demonstrate resilience, and jobless claims provided important context. Here's an in-depth review of the week's top stories:

What "Fueled" the Rise in Consumer Inflation?

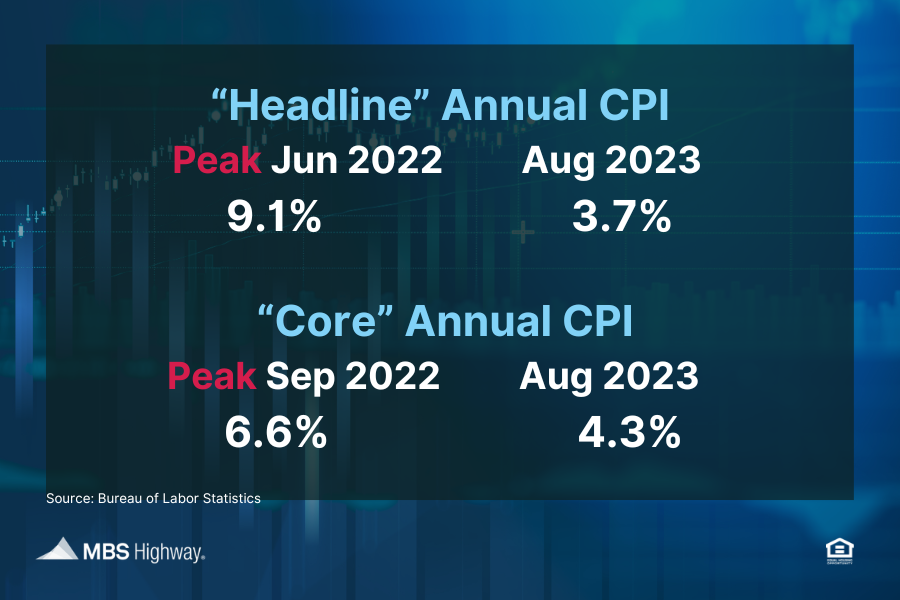

The Consumer Price Index (CPI) for August made headlines as it revealed a 0.6% increase, aligning closely with market expectations. On an annual basis, CPI climbed from 3.2% to 3.7%. Despite this uptick, it's important to note that inflation remains near its lowest point in over two years. Core CPI, which excludes volatile food and energy prices, grew by 0.3%, while the yearly reading dipped from 4.7% to 4.3%.

The surge in energy and gasoline prices was a primary driver behind the monthly inflation uptick. In contrast, stable food and shelter prices, coupled with reduced costs for used cars, contributed to moderating inflation last month. An interesting caveat is the potential impact of the United Auto Workers strike on new car supplies, which could result in rising used car prices.

Bottom Line: While wholesale inflation also experienced an upward shift, it's essential to consider that these changes started from a notably low point and remain subdued, far below the peak of 11.7% witnessed last year. Furthermore, New York Fed President John Williams emphasized that inflation could have been even lower if declining shelter costs were more promptly factored into the reporting.

Is the Rise in Wholesale Inflation a Concern?

The Producer Price Index (PPI), measuring inflation at the wholesale level, startled economists with a 0.7% surge in August, surpassing expectations. On an annual basis, PPI doubled, rising from 0.8% to 1.6%. Core PPI, excluding volatile food and energy prices, saw a 0.2% increase, with the yearly reading declining from 2.4% to 2.2%.

Bottom Line: The rise in wholesale inflation, while notable, must be viewed in the context of its low starting point. It remains significantly muted, especially when compared to last year's peak of 11.7%. The Federal Reserve has been employing a series of interest rate hikes to curb inflation and stabilize the economy. Recent statements from several Fed members suggest a potential pause in rate hikes, given the progress in curbing inflation. The final decision rests with the Fed, with their upcoming meeting providing valuable insights.

New High in Home Price Appreciation

CoreLogic's Home Price Index reported a consistent upward trajectory in home prices, marking the sixth consecutive monthly increase of 0.4% from June to July. Compared to the same period last year, home prices surged by 2.5%. CoreLogic's forecasts project a 0.4% rise in August and a 3.5% increase in the year ahead. It's worth noting that these forecasts have historically leaned towards conservatism. In fact, based on the monthly gains thus far in the year, CoreLogic's index is on track for an impressive 9% appreciation in 2023.

Zillow echoed these sentiments, reporting a 4.5% increase in home values since the beginning of the year, reaching new all-time highs since May. Zillow's index points to a potential 7% appreciation by year-end, given the current monthly growth rates.

Bottom Line: The continued surge in home prices aligns with reports from Case-Shiller, Black Knight, and the Federal Housing Finance Agency. These consistent findings emphasize the appeal of homeownership as an opportunity for wealth accumulation through real estate investments.

Important Context Regarding Tame Jobless Claims

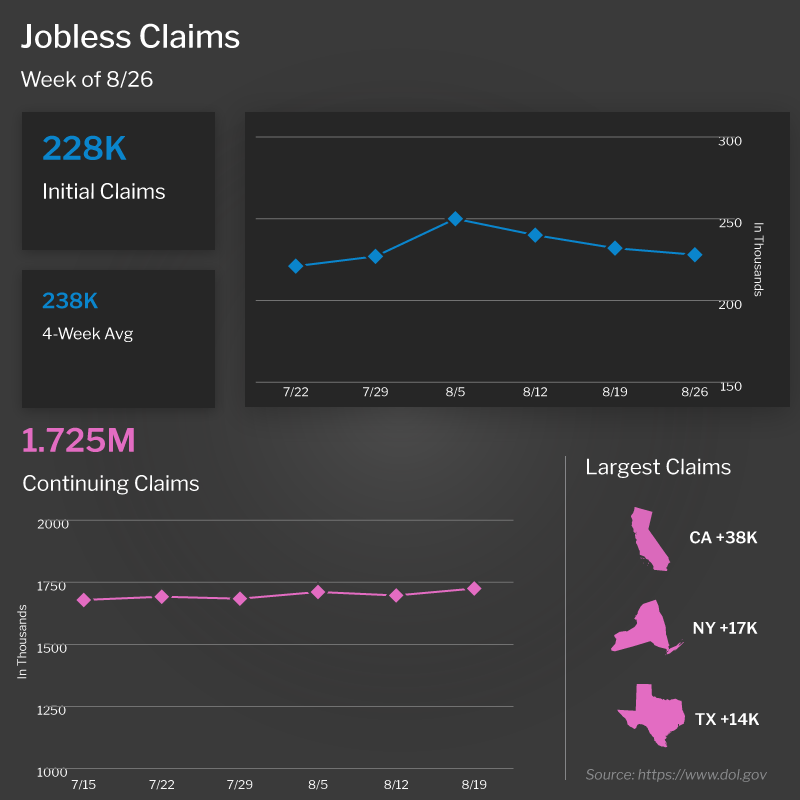

Initial Jobless Claims increased by 3,000 in the latest reporting week, with 220,000 individuals filing for initial unemployment benefits. Continuing Claims rose by 4,000, with 1.688 million people continuing to receive benefits after their initial claim. It's essential to note that this number has been on a downward trajectory since early April when it reached a peak of 1.861 million. This decline reflects a mix of individuals finding new employment opportunities and the expiration of benefits.

Bottom Line: While Initial Jobless Claims may suggest a robust labor market, it's important to consider the context. The measured week included the Labor Day holiday, which may have affected filing times and influenced the data. Initial Jobless Claims are typically the last indicators to reflect a labor market slowdown. Initial signs are usually observed through decreases in job postings, hirings, and reduced working hours. Recent reports have indicated these initial trends, and it will be crucial to monitor for a sustained increase in Initial Jobless Claims, especially as the Fed considers further rate hikes this fall.